freelance budgeting

Freelance Budgeting: A Simple Monthly System That Works

Get a clear, monthly freelance budgeting system. Know what to save, what to spend, and when to send invoices so cash stays steady.

Freelance budgeting is the part most people skip—until rent is due and the bank balance looks nothing like the “good month” they remember. The fix is not more hustle. It’s a simple system that tells you what money is coming, what money must leave, and what’s safe to spend.

The problem with “winging it” as a freelancer

Most freelancers don’t struggle with making money. They struggle with timing.

Income often comes in bursts: a big invoice paid late, a small retainer that hits on time, a project that closes over a few weeks. Meanwhile, expenses don’t pause. Insurance, software subscriptions, taxes, and personal bills keep arriving on schedule.

That’s why budgeting for freelancers is different from budgeting for a salaried job. Your goal is cash flow control, not just tracking spending.

Set up your freelance budgeting system (one hour to start)

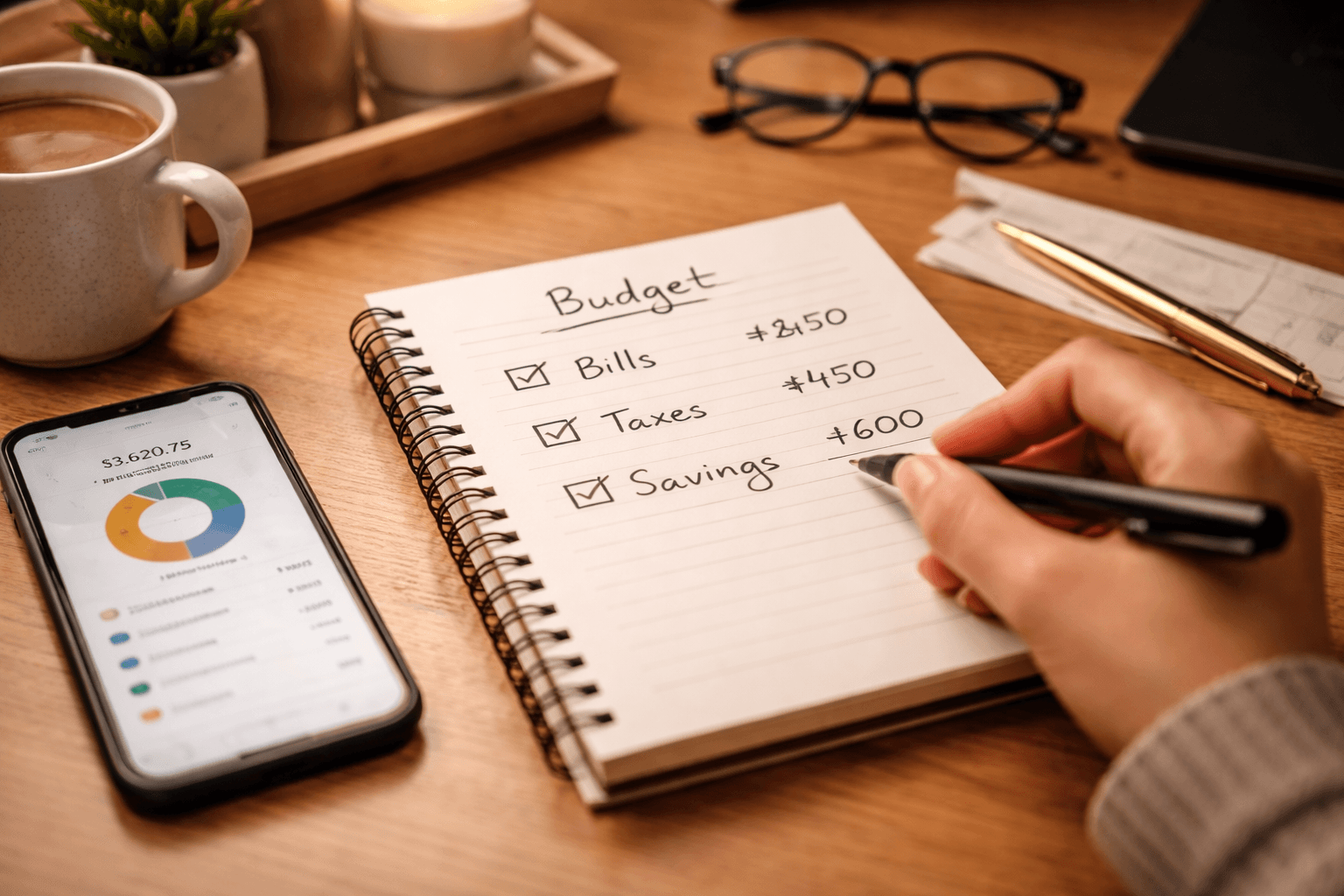

Think of your budget as three buckets plus one habit.

1) Bucket A: “Must-pay” bills

Start with the expenses that cannot wait. These are your survival costs.

Include things like:

- Rent or mortgage (or your home office portion)

- Utilities and internet

- Health insurance and other recurring coverage

- Minimum debt payments

- Core tools (e.g., design software, cloud storage)

If a bill is due monthly, put it in a monthly number. If it’s due quarterly, convert it to a monthly equivalent.

2) Bucket B: Taxes (pay yourself like a contractor)

Even if you’re good at saving, taxes can still sneak up if you don’t plan for them.

Rule of thumb: set aside a percentage of revenue for taxes, then adjust based on your local tax situation and your accountant’s advice.

To make this practical:

- Pick a tax set-aside rate you can live with

- Track it per project (or per invoice)

- Move money to a dedicated “Taxes” bucket when invoices are paid

This turns tax prep from an annual scramble into a monthly process.

The goal isn’t perfect math. It’s reducing the chance you owe money you didn’t plan for.

3) Bucket C: Personal + business spending

Now decide what you can spend without risking your bills.

Personal spending includes groceries, transportation, subscriptions, and anything you want to enjoy. Business spending includes growth items like courses, marketing experiments, hardware, and hiring help.

A common mistake is treating “whatever is left” as your spending plan. In freelancing, “whatever is left” is usually a trap because invoices arrive late.

4) The one habit: monthly money review

Do this once per month (30–45 minutes). You’re answering four questions:

- How much cash do I have today?

- How much is coming in by next month?

- What must leave before then?

- What’s safe to spend or invest?

Once you can answer those questions, budgeting stops being stressful.

Build your “cash calendar” for the next 30–60 days

Freelancers don’t need a yearly budget as much as they need near-term clarity.

Create a simple calendar with the next 6–8 weeks. Add:

- Incoming: each expected invoice payment date (or best guess)

- Outgoing: each bill due date

- Holds: the tax set-aside amount you plan to reserve

Then do a quick stress test.

Stress test: assume 1 payment is late

Pick your most likely risk (late client, slower approval, extended review cycles). Assume that invoice slips by 2–3 weeks.

Ask: Can you still cover your must-pay bills?

- If yes: good. Your system is resilient.

- If no: you need to adjust now. That can mean slowing discretionary spending, tightening payment terms, or choosing a different project mix.

This is where freelancers usually find out their “budget” was really a hope.

Use a simple workflow to connect budgeting with invoicing

Budgeting fails when it’s disconnected from your operations. You need the budget to reflect your real work and payment timing.

Here’s a practical workflow you can run every time you send an invoice.

-

Estimate the expected payment date

- Add a buffer based on your past experience with similar clients.

-

Assign the money to buckets immediately

- “This invoice revenue is for bills, taxes, and (maybe) spending.”

-

Send a short payment reminder schedule

- For example: reminder at 7 days, then again near the due date.

-

Track follow-ups as part of cash planning

- If you’re budgeting for next month, your follow-ups are part of the “income coming” picture.

If you want to sanity-check your whole operation, run the Freelance Business Check and look for common cash and process blind spots that show up in budgeting.

Common freelance budgeting mistakes (and how to fix them)

Mistake 1: Mixing business and personal cash

When your accounts are tangled, it’s hard to know what’s safe.

Fix:

- Use separate buckets (even if it’s just separate spreadsheet sections or a dedicated bank account for taxes)

- Treat client payments as business cash until the money is allocated

Mistake 2: Ignoring taxes until the end of the year

Fix:

- Set the tax set-aside rate now

- Reserve it whenever an invoice is paid

- Revisit the rate once you have better data (or with your accountant)

Mistake 3: Planning based on revenue, not payment

“Expected revenue” doesn’t cover bills. Cash does.

Fix:

- Build your cash calendar from payment dates

- Use conservative timing when you forecast

Mistake 4: No buffer for irregular projects

Freelancing has quiet months and busy months.

Fix:

- Create a “buffer” bucket: a monthly target you build over time

- If a month is lean, reduce discretionary spending rather than panic-cutting everything

Mistake 5: Not adjusting when scope creeps

Scope creep (extra revisions, added deliverables, “one more thing”) increases time but often doesn’t increase income.

Fix:

- Track deliverables per agreement

- If something changes, confirm it in writing and update the schedule and price

A budgeting system works best when your pricing and scope stay stable.

Make it easier: templates you can reuse

You don’t need a fancy spreadsheet. You need a repeatable structure.

Try this budget template each month:

- Must-pay bills total

- Tax reserve target (tax rate × paid invoice revenue)

- Discretionary spending limit

- Buffer contribution (even if small)

- Total “safe to spend”

Then update it during your monthly money review.

If you want a tool approach, the key is centralizing your client work so you can tie proposals, contracts, invoices, and messages to your cash plan. When client info and payment status live in one place, follow-ups and forecasting get easier.

Related reading: Freelance Time Management Playbook: Weekly System · Freelance Pricing That Works: A Repeatable Method

Conclusion: budgeting is just decision-making with fewer surprises

Freelance budgeting doesn’t need to be complicated. Your system only has to answer one question every month: “Will my cash cover what’s due, and what can I safely spend?”

Start with must-pay bills, reserve for taxes, and plan around payment dates. Then do one monthly review and one cash stress test. Within a couple of cycles, you’ll feel the difference.

If you’d like help keeping proposals, contracts, invoicing, and client messages in a cleaner workflow, Jolix can centralize your freelance operations so budgeting stays connected to what’s actually happening with clients.